One of the most common questions across higher education throughout the past year has been: how can we further diversify our international student population?

For highly ranked institutions globally, there is a common need to reduce reliance on China. In May, it was reported in the UK that the Office for Students (OfS) wrote to 23 institutions over ‘high levels’ of Chinese students, encouraging them to have ‘contingency plans’ in case of a ‘sudden drop’ in numbers.

Comparably, many mid-to-low ranked institutions around the globe have become overly reliant on the Indian market, particularly for postgraduate recruitment. This is evidenced by more than 170,000 Canadian study permits being issued to India in 2021*, more than three times the volume of the second biggest source market, China. In the UK, for institutions outside the top 200 of the THE World Ranking, India accounted for more than 40% of PGT enrolments in the 2021/22 academic cycle.**

* IRCC, CDO Temporary Residents January 31, 2022 data

** HESA international enrolments 2021/22

The importance of these two markets is clear. But the question emerges: which other markets outside of China and India should we be paying attention to?

Our IDP IQ team of data scientists and higher education research professionals, has been exploring which international source markets to keep an eye on going into 2024 with a focus on emerging markets in Africa.

Source market population and economic growth

The IQ team at IDP produces five-year forecasts for institutions’ international recruitment based on historical enrolment trends, in addition to key market variables that highly correlate with market recruitment volume. When looking at undergraduate recruitment, two of the variables that we see having the highest correlation with historical recruitment volume from a given market are population growth and GDP.

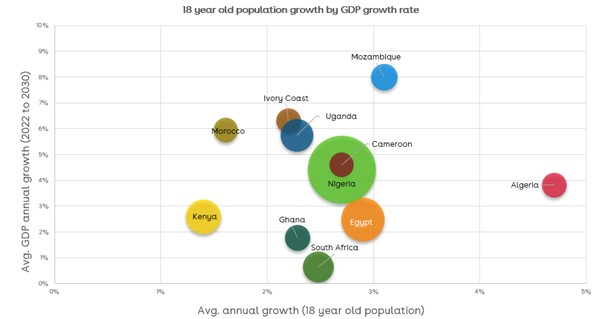

In the below chart, we’ve looked at the key Africa source markets with high 18-year-old population growth and growing GDP. The average annual growth rate of the 18-year-old population between 2022 and 2030 is plotted on the X-axis and the forecasted average annual growth rate of GDP on the Y axis. The size of the bubbles reflects the size of the source market population, based on 2022 UN data.

Within the top 30 source markets for recruitment into the UK, Australia and Canada, the country with the highest 18-year-old population growth between now and 2030 is Algeria –

and that is globally, not just within Africa – and this demographic is set to grow by an average of 4.7% year-on-year. In addition, Algeria’s GDP annual growth rate, forecast by the International Monetary Fund, is also predicted to grow by 3.8% annually on average up to 2028 (which is as far as the IMF projects).

The gross enrolment rate in tertiary education in Algeria is also growing, having been reported at 54% in 2021, up from 37% in 2015. Algeria is already the third largest African source market for Canada, after Nigeria and Morocco. Whilst current volumes to the UK are low, with only 270 enrolments (HESA) in 2021, the population and GDP indicators point to Algeria being an emerging market over the next 5-10 years.

Nigeria, a more established source market for many institutions, is growing in importance and is set to see increasing volumes of 18-year-olds over the remainder of this decade. However, devaluation of the Naira and climbing annual inflation, which rose to 25.8% in August 2023, have created challenges with application-to-enrolment conversion from this market as students become increasingly price sensitive.

Egypt is also a market with growing recruitment potential based on the increasing student population. Almost 20% of Egyptians are aged 15-24 and their population of 18-year-olds is set to grow by an average annual growth rate of 3% year-on-year from 2023 to 2030. However, similar to Nigeria, they face challenges with inflation, and Egypt's annual urban consumer price inflation rose to a historic high of 38% in September 2023.

Whilst Mozambique is set to see significant population and GDP growth, this is not historically a strong market for recruitment, with only 25 students recorded from this market to the UK in 2021/22 (HESA).

Overcoming barriers for recruitment growth

The key theme across all these markets is price sensitivity. Higher education institutions will need to consider how they can overcome price barriers on course fees, accommodation and living costs in order to capitalise on the growing student populations in these source markets.

IDP IQ can overlay this data with institution market share and historical enrolment trends to produce international enrolment forecasts. Contact us for more information about how IDP Connect can support your institution with international recruitment forecasting and strategic planning.

You might like...

What Influences Today's Students?

Using data compiled over the last 18 months, IDP explores what factors are influencing today's students

GLOBAL PRESS RELEASE: Emerging Futures, Voice of the International Student

US takes pole position in the eyes of international students whilst Australia takes second place

Indonesia: The Rising Source Market of Southeast Asia

Our latest regional source market report focusing on Indonesia as a growing diversity market